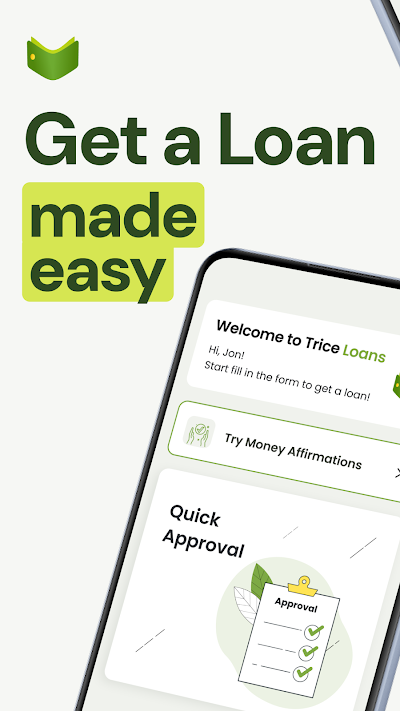

About Payday Cash Advance TriceLoans

Let me be honest: I downloaded TriceLoans with a fair bit of skepticism. My dog needed an emergency visit, and my paycheck was still a week out. I’d seen ads for these apps before, but I needed something real. TriceLoans isn’t a magic fix, but for that specific, tight spot, it was a legitimate lifeline. This review is based on my actual experience using it to cover that $300 bill.

Features & Highlights

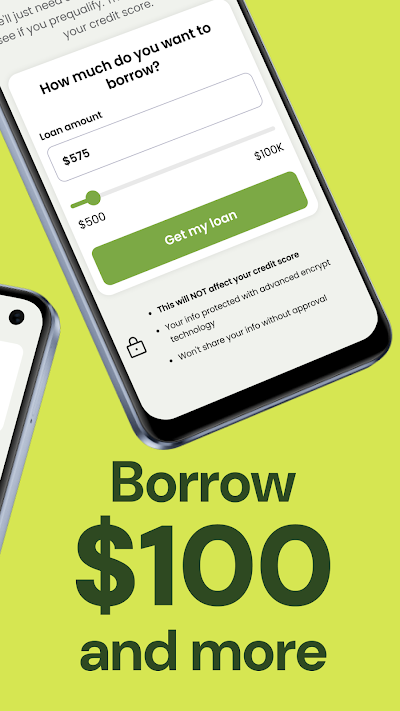

The app does a few things very well, which is what matters in a panic. The approval speed is its biggest sell. I submitted my application around 10 AM and had a “conditional approval” by 10:20 AM. It wasn’t just a quick “yes,” though; they asked for a recent pay stub and bank statement link through a secure portal, which felt more thorough than I expected. I like that you can choose your loan amount in specific increments—I borrowed exactly what I needed for the vet, not a forced, larger sum. The repayment schedule tool is clear; I could slide a bar to see how different payoff dates affected the total cost. While I didn’t need it, seeing a “Contact Support” button right on the main dashboard gave me some peace of mind.

User Experience

Navigating the app when you’re anxious is the real test. The design is simple, almost plain, which worked in my favor. No confusing menus. I remember the moment I linked my bank account—it used one of those verified, read-only connections (like Plaid), which felt safer than typing in my login details manually. The waiting screen after submission showed a progress bar, which was a small touch that stopped me from refreshing constantly. When the funds hit my account later that afternoon, I got a push notification and an email simultaneously. Repaying was straightforward; I scheduled the payment for my payday right within the app, and it just happened automatically.

Pricing

The app itself is free to download and use. The cost comes from the loan fees, which are clearly displayed before you finalize anything. For my $300 advance, the fee was $36, which is steep if you think of it as an annual rate, but as a flat fee for a 10-day bridge, I understood the trade-off. They are transparent—there were no hidden charges, and the total due was on every screen. Is it worth it? For a genuine, urgent, short-term cash gap when you have no other options, yes. As a regular thing? Absolutely not, and the app doesn’t encourage that.

Updates & Support

Looking at the update history in the App Store, the developer pushes small bug-fix updates every 3-4 weeks, which suggests they’re maintaining it. I had one question about the document upload, so I used the in-app chat on a weekday afternoon. A real person named Maya responded in about 15 minutes with clear instructions. It wasn’t 24/7 support, but it was competent and human, which is a lot better than a bot or a FAQ page.

Security & Privacy

I downloaded TriceLoans directly from the Google Play Store. Their privacy policy is linked upfront during sign-up, and it states they don’t sell personal data to third-party marketers. The app uses encryption for data in transit, and linking my bank via the secure third-party service was reassuring. I didn’t encounter any ads within the app itself, which was a relief. My main privacy concern is inherent to any loan app: you have to share very sensitive financial data. TriceLoans felt as secure as it could for that process, but it’s a big thing to trust any app with that info.